KANSAS CITY, MISSOURI, US — If 2022 taught us anything, it was to expect the unexpected. It was the year that shocked us with war in Ukraine, endless Chinese COVID-19 lockdowns, soaring inflation and extreme weather, including in the United States where Mississippi River levels dropped to record lows. It also, finally, saw the world stride toward a post-COVID future, even as large swathes of the global economy teetered on recession.

Those in the business of buying bulk carrier capacity have had their own surprises, not just in 2022 but throughout the pandemic — not least because they could have expected freight costs to subside more significantly than they have given the mismatch between fleet and volume growth.

“In the four years since 2018 the dry bulk fleet has expanded by 15%, but the volume of cargo has only expanded by 2.9%,” said Will Fray, director at Maritime Strategies International (MSI). “Even tonne-miles have only increased by 3.5% over this period.”

So, what has been bridging the gap between supply and demand growth? Fray said port congestion caused by COVID supply chain disruptions has been “absolutely critical” to the strength of the freight market through 2021 and 2022. Indeed, he argued, congestion has been the prime driver of pricing. Quite simply, rates through the period “cannot be explained otherwise,” he said.

The port congestion equation

By tying up large chunks of the global bulk carrier fleet, port congestion has helped offset slow demand growth by taking effective capacity out of the market, which has inflated returns for ship owners but added to freight and charter costs for shippers.

“We estimate the positive impact of various fleet inefficiencies on market balances in 2021-22 to have been equivalent to the iron ore trade between Australia and China,” Fray said.

However, any reduction in port congestion could see freight and charter costs slump.

“When this support is removed as COVID-related inefficiencies subside, the freight market will come under pressure,” Fray said.

“We expect an 8% decline in grain exports from the US in 2023. US grain exports were 20% down in the first half of 2022 as compared to the first half of 2021.” - Tanvi Sharma, research analyst, Drewry

This process is already underway. Port congestion at Chinese ports has fallen for most ship categories during 2022, although the numbers still in queues remain substantial. At least 800 ships have been tied up at Chinese ports every week during 2022 and, in some weeks, that number has surpassed 1,000 vessels, according to Breakwave Advisors. In late November, in the less-than-capesize fleet segments used for shipping grains, some 239 panamax, 280 supramax and 171 handysize vessels were caught up in congestion in China.

Should this congestion ease, as many expect it will during 2023 — and particularly if China loosens its zero-COVID policies — then bulk carrier freight rates could tumble, especially as dry bulk volumes are expected to grow by just 1.6% in 2023, according to MSI.

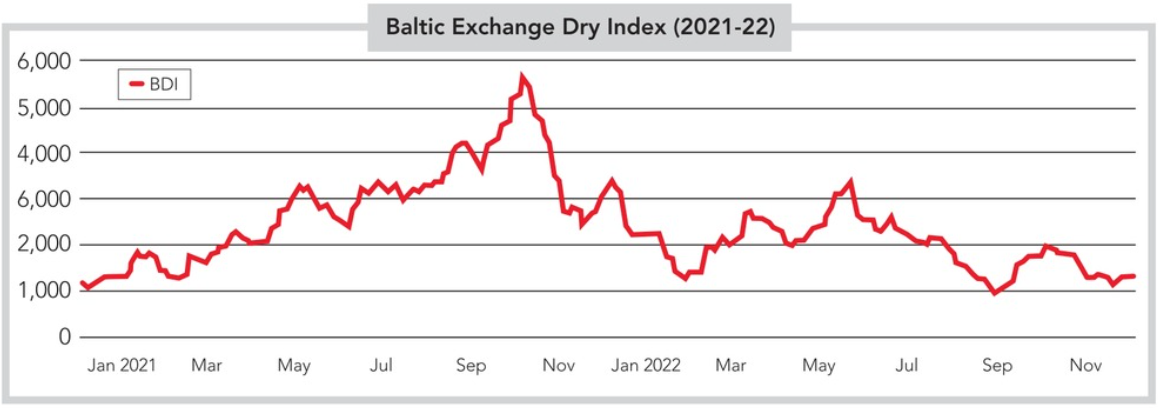

Indeed, rates already have dropped significantly from the highs of 2021. The Baltic Dry Index (BDI) reached 5,650 points in October 2021, a two-year high, but had dropped to just 1,323 on Dec. 5, 2022. The Baltic Panamax Index (BPI) was down to 1,638 on Dec. 5 compared to a two-year peak of 4,328 in October 2021, while the Baltic Handysize Index (BHI) hit 732 in the first week of December, down from a two-year high of 2,062 in October 2021.

Similar declines are apparent in grain shipping costs. On Nov. 29, the International Grains Council’s (IGC) Grains and Oilseed Freight Index (GOFI) fell to 148 compared to a year-high of 243 points recorded in May. Year-on-year drops of between -27% and -32% were apparent across the IGC’s sub-indices in the last week of November.

Vessel demand and supply

There is little on the fleet growth side to prevent a drop in congestion from delivering lower grain shipping costs next year. Bimco expects fleet growth of just 2.1% in 2023, but even this will outstrip anticipated volume expansion.

“Demolition is expected to increase in 2023 as environmental regulations and an economic downturn could lead older tonnage to be recycled,” the analyst said. “Nonetheless, despite an aging fleet, total demolition should remain under 15 million dwt due to the small orderbook.”

Ship owners have started to cut sailing speeds to help reduce overall vessel availability. However, this is proving insufficient to buoy rates.

“Congestion started to clear in the second half of 2022,” Bimco said. “As of November, it is down 4.8% year-on-year. In response to a cooling market and a higher bunker price, average sailing speed closed in on 11 knots and is now down 4.5% for laden ships and 2.4% year-on-year for ballast ships.

“Despite a drop in sailing speed, this has been insufficient to compensate for the easing of congestion, and the supply/demand balance has worsened (for ship owners) as a result.”

In 2023, Bimco expects both sailing speed and congestion to remain low due to limited cargo demand growth and new International Maritime Organization (IMO) Energy Efficiency Existing Ship Index (EEXI) regulations that enter force Jan. 1, 2023, and are designed to cut emissions.

Bulk carrier demand growth is due to be slow at 1.6% in 2023 due to the more general global downward trend in economic indicators across major economies. This growth is being reinforced by tighter fiscal and monetary policies as policymakers continue to target high inflation.

“Importantly for the dry bulk markets, this implies continuing pressures for the property sector and for durable goods demand sectors, which are typically sensitive to financing conditions,” MSI said.

The China question

China is always critical for the dry bulk trades and could well be the key to any major change in outlook given the pull-effect that steel and iron demand has on rates for the smaller, sub-capesize ships used by grain shippers.

After protests in China in late November against President Xi’s strict lockdown policies, there are signs that his zero-COVID strategy could soon be eased. Official encouragement was given to regional administrators to avoid full lockdowns and reduce regular PCR tests in December, while Xi was reported to have told visiting European Council President Charles Michel that the Omicron variant was less lethal than previous variants and his government was going to ramp up its vaccination program.

“Over the past couple of days, a number of large cities — including Beijing, Shanghai, Guangzhou and Shenzhen — scrapped negative PCR test result requirements for public transport,” said Nomura in early December. “Overall, we believe China is discouraging full-city hard lockdowns and taking steps to loosen the overly restrictive COVID curbs, especially the massive regular PCR tests. However, many other cities have yet to catch up, and some cities have even recently introduced new PCR test requirements, suggesting the central government has not given clear and direct instruction yet and local governments are still confused.”

Any opening up of China’s economy could spark economic activity back into life and drive dry bulk demand. Capesize rates are driven primarily by the steel industry and shipments of iron ore and there were signs that Chinese demand was increasing during November when Chinese crude steel output and prices increased. Breakwave Advisors predicted that China’s steel output likely bottomed out in late July and noted that stockpiles have continued to decline.

MSI believes that any improvement in China’s property sector or a relaxation of China’s zero-COVID policy “has the potential to boost demand significantly and presents a clear upside risk to trade.”

“Progress, however, is likely to be incremental and take a number of months, especially as we currently see a significant increase in COVID-19 cases across China,” the analyst added. “Until such progress, the freight markets need to contend with the outlook for what could be particularly weak trade in Q1 2023.”

The Black Sea

Credit: Baltic Exchange

Credit: Baltic ExchangeOf course, the grains shipping market has been subject to its own particular travails in 2022, not least because war in Ukraine has limited exports via the Black Sea and record-low water levels on the Mississippi River have stymied the US market.

The Black Sea Grain Initiative (BSGI) has now been extended into 2023, although exports continue to suffer delays, tying up bulk carriers as they await clearances and inspections.

“Despite the renewal of the grain deal, de-congestion in the region is crucial for the shorter journey of vessels,” said Tanvi Sharma, research analyst at Drewry. “Recently, many ballast vessels had to undergo inspections that were delayed by as many as nine days, while the waiting time of laden ships stretched for two weeks in Turkey. As the winter sets in, resolution of such bottlenecks by the Joint Coordination Centre is essential for continued supply of grain in the market.”

Sharma believes that Ukraine’s importance as a grain exporter makes the ongoing viability of the BSGI critical.

“There is a lack of alternative modal routes for this trade,” Sharma told World Grain. “Several European economies, such as Ukraine and Russia, have broad gauge railway tracks while others have narrow gauge tracks. Since Poland falls in the latter category, any exports from Ukraine to Poland will be through the broad gauge and thereafter the cargo will have to be reloaded on the Euro rail gauge, increasing the cost and rendering the transport mode inefficient and uncompetitive.

“At the same time, war prevents significant exports via roads, which in any case is a costly logistics solution for bulk cargo. This leaves stakeholders relying on seaborne trade.”

This is essential for owners of mid-sized vessels that cater to the grain market. Any change in the market conditions affects the supply of crew, insurance, journey time as well as risk in the market. All in all, freight cost is impacted.

Mississippi River problems

In the United States, it will take some time for exporters to recover from lower water levels during 2022, added Drewry’s Sharma.

“The hampering of exports in the third and fourth quarters of 2022 from the US Gulf due to low water levels on the Mississippi River is impacting grain exports in the peak season,” Sharma said. “Waiting time for vessels has risen due to disrupted inland waterway connectivity. Such bottlenecks have a significant impact on the supply of grain as well as shipping supply and demand.”

Rates forecast for 2023

The upshot of all of which is likely to be falling bulk carrier rates in the first part of 2023 with grain supplies limited from key sources.

Sharma said the impact of the Russia-Ukraine war was likely to place a ceiling on supply from the Black Sea, while the US harvest forecast did not look promising for the next year.

“We expect an 8% decline in grain exports from the US in 2023,” she added. “US grain exports were 20% down in the first half of 2022 as compared to the first half of 2021. USDA estimates a significant drop of about 11% in coarse grain exports in 2022-23, even though the drop in wheat exports is a minor 1% in the same period.”

As a result, Drewry expects “charter rates to decline in 2023.”

Bimco added that in 2023 weather conditions could continue to be a disrupting factor as La Niña occurs for a third consecutive year, affecting mining and agriculture globally.

“Based on the IMF’s base case economic forecast and the market outlook for the three major bulks, we expect that freight and time charter rates will remain weaker than those seen during 2021 and the start of 2022,” said the analyst, adding that rates could increase in the second half of next year if economic conditions improve.

Bimco added: “The Chinese government will remain a wildcard, as their economic policy retains the potential to boost bulk demand.”

For his part, Fray expects the availability of tonnage to improve in 2023 as congestion eases, pushing freight rates down.

“This is even after taking into account an uptick in Chinese import demand on the back of more economic stimulus and a marginal slowing of the fleet due to EEXI regulations — factors that have convinced some other analysts that the dry bulk freight market will be strong next year,” he said. “In effect we believe that the negative effect on freight rates of an unwinding of COVID-related inefficiencies will more than offset a basket of positive factors.”

Michael King is a multi-award-winning journalist and podcaster as well as a shipping and logistics consultant. He also supplies an array of corporate services. For more information, email mikeking121@gmail.com.